How many times have you heard that what you don’t know can’t hurt you? Actually, what you don’t know can hurt you – just ask any taxpayer who has tried to persuade the IRS not to hold them accountable for an error on their tax return because they didn’t realize it was an error.

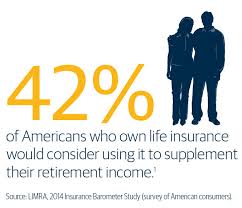

Clients who don’t realize life insurance can be leveraged for tax diversification in a retirement plan may suffer negative financial impacts due to what they don’t know. Although many permanent life insurance policies can help diversify a retirement plan, innovation in index universal life (IUL) insurance has brought about the potential to provide protection, supplemental retirement income and long-term wealth accumulation, typically with no tax penalties on properly structured distributions at any age.

Clients’ money at work for them

Unlike the limited contribution levels of IRAs and 401(k) plans, there are few limits to the amount of money clients can put to work in a life insurance strategy, although cash value policies are subject to Modified Endowment Contract rules that discourage overfunding based on face amount, the insured’s age and other factors (more on that to come in a moment). Cash value life insurance also contains additional mortality charges that will increase the expense of the product, and this factor is among the reasons why a policy illustration should be consulted for more information. However, there are no income-based participation restrictions and the tax-free life insurance death benefit may help ensure the client’s objectives are achieved, even if the client dies sooner than anticipated.

A flexible IUL product, which provides a greater potential for interest than a traditional universal life policy, may fit the bill for clients seeking safety and the potential for cash value growth. That’s because, although IUL is an insurance product rather than an investment, it provides cash value growth potential through index-linked interest credits. Clients do not invest in an index directly; rather, growth potential in IUL cash values is linked to market index performance, with guaranteed floors protecting against loss in down markets. (All guarantees are backed by the claims-paying ability of the issuing insurance carrier.) Furthermore, IUL supports the power of tax diversification for clients’ retirement portfolios.

Tax treatment of retirement assets

Many people understand the benefits of diversifying investments among asset classes to manage risk and return in a retirement plan. But diversification can also be used to manage the tax treatment of retirement assets, resulting in the potential for higher net income during retirement years.

If the client’s objectives include minimizing tax exposure every year, he or she may want to allocate assets among various types of financial products/accounts where asset growth is taxed at different rates and times. It may be helpful for the client to be able to discern among assets that are taxed later, such as 401(k) accounts; mutual funds that are taxed now; and solutions such as life insurance, the cash values of which may never be taxed.

It may also be helpful to walk clients through a comparison of the features of various financial accounts/products, including life insurance policies, that may be part of an overall balanced retirement plan. Among the features that may make cash value life insurance particularly attractive are tax-deferred accumulation, an income-tax free death benefit for beneficiaries, different IRS limitations on premiums paid than on contributions to qualified plans, the potential for missed premiums to be “made up” at a later time, income-tax free distributions (when properly structured) using withdrawals and loans, and client access to cash values prior to age 59½. These features are contingent, of course, on the policy complying with IRS requirements to qualify as a life insurance contract. Additionally, total premiums in the policy cannot exceed funding limitations under IRC section 7702.

Under some circumstances, withdrawals from the contract may be treated as income first and includible in the policyholder’s income. For example, if the policy is classified as a Modified Endowment Contract (see IRC section 7702A), withdrawals or loans are subject to regular income tax to the extent there is any gain in the policy. Also, an additional 10 percent tax penalty may apply to the taxable portion of those policy distributions if they are taken prior to age 59½. Note that distributions will reduce policy values and may reduce benefits; and the availability of policy loans and withdrawals depends on multiple factors, including, but not limited to, policy terms and conditions, performance, and fees or expenses.

Nonetheless, clients may appreciate the opportunity to leverage the advantages an IUL policy provides for a tax diversification strategy of retirement assets. While a 401(k) alone has merit, it may not have enough.

Consider an example

Consider the following hypothetical example, which is for illustrative purposes only.

In addition to some rental income, Fergus and Oriana Epstein have all of their retirement assets in a 401(k) plan. They’ve maximized their contributions and have a tidy sum saved for their retirements. However, their withdrawals will be taxed as ordinary income. Their financial professional pointed out that since the Epsteins are currently in the 25 percent tax bracket, their planned annual withdrawal of $100,000 would result in taxes of $25,000, leaving a net distribution of $75,000 for their retirement income. Keep in mind that withdrawals are subject to federal income tax and may be subject to state income taxes. Also, a 10 percent federal early withdrawal tax penalty may apply if taken before age 59½.

After the recent review with their financial professional, it was determined that cash value life insurance could not only provide death benefit protection, but also provide tax diversification advantages. The financial professional recommended that the Epsteins purchase a $1 million IUL policy to protect the family. Their financial professional showed the couple how an IUL can help them meet both objectives – life insurance protection for their family and an asset to increase their diversification.

Suppose the Epsteins choose to take a $50,000 distribution from each of the financial product “buckets.” Based on a 25 percent ordinary income tax on the 401(k) withdrawal, resulting in after-tax distribution of $37,500; and a $50,000 income-tax free loan from the IUL policy, the total net income from the $100,000 gross distribution would be $87,500, which is $12,500 more than with the 401(k)-only plan.

Potential clients

Both asset diversification and tax diversification can be of critical importance in retirement income planning. With its attractive attributes, the type of IUL solution available today may serve as a key component in building a successful retirement strategy for clients, particularly individuals and small business owners who are ages 35-55 and:

- are seeking accumulation and tax-protected gains for retirement income, college funding or other cash needs

- want to supplement a traditional/Roth 401(k), IRA or 529 plan

- have higher income or are affluent with investible assets, and

- are less risk tolerant than buyers of variable universal life (VUL) insurance, but are still willing to accept some risk.

An alternative solution

Other clients may also be seeking the opportunity for cash value growth, but prefer an IUL solution that’s more focused on guaranteed protection. In the current IUL marketplace, it’s also feasible to offer an IUL product that’s designed to provide an economical alternative to a guaranteed universal life (GUL) product, while providing death benefit protection for income replacement, wealth transfer or estate planning.

Perhaps it’s time to change that old adage to, “What you do know can help you.”